How to Rebalance Your Solana Portfolio: Complete Guide (2026)

How to Rebalance Your Solana Portfolio: Complete Guide (2026)

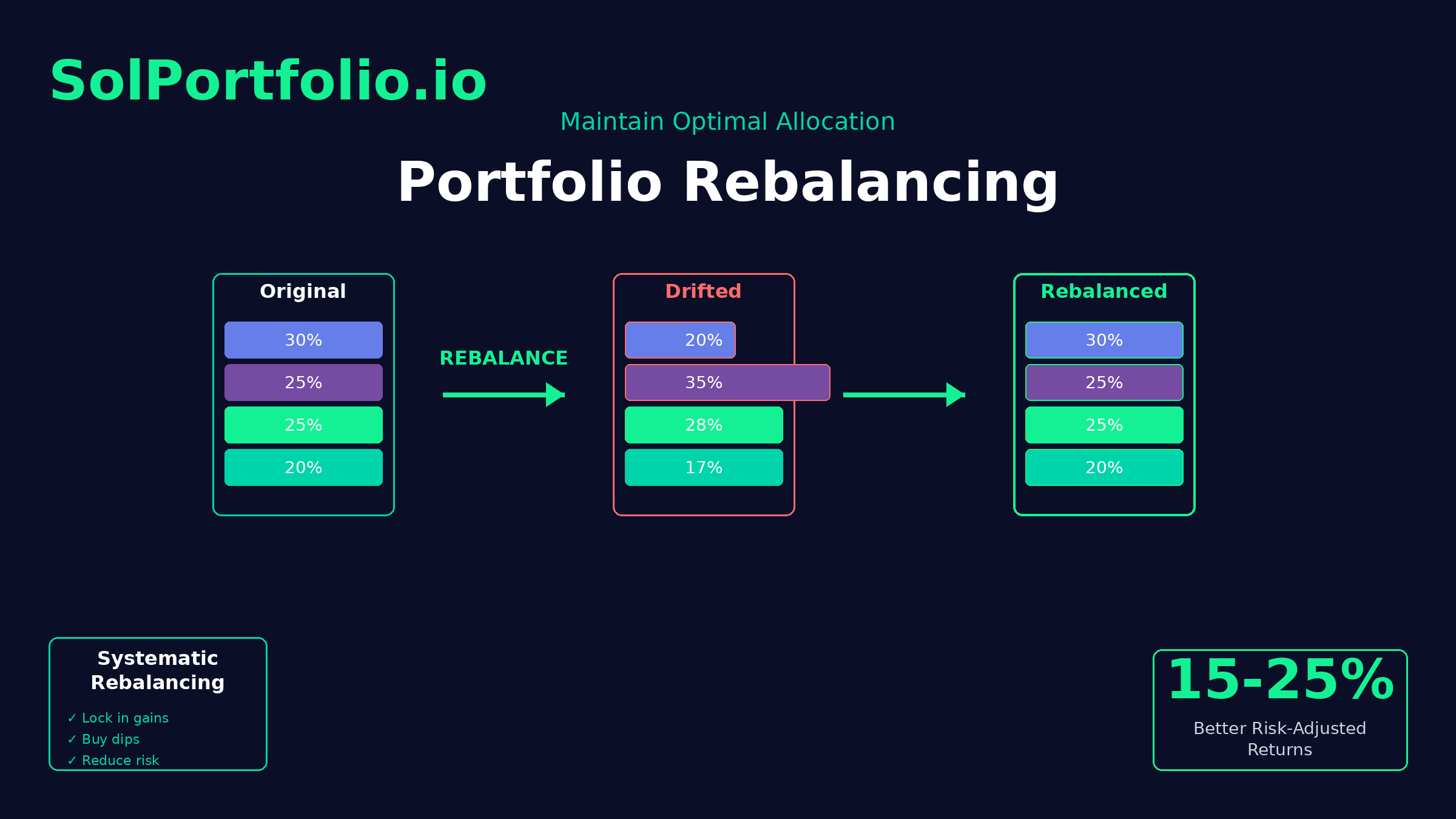

Your Solana portfolio looked perfect three months ago. You had the right allocation, everything was balanced. But today? One token has exploded 200%, another has dropped 40%, and your carefully planned allocation is completely off track. You’re now overexposed to volatile tokens and underweight in stable performers. This is portfolio drift—and it’s costing you money every day you ignore it.

Portfolio rebalancing is the disciplined process of realigning your holdings back to your target allocation. For Solana investors, regular rebalancing can improve risk-adjusted returns by 15-25% compared to passive portfolios. This comprehensive guide shows you exactly when, why, and how to rebalance your Solana portfolio for maximum returns while minimizing risk and tax impact.

What Is Portfolio Rebalancing?

DEFINITION: Portfolio rebalancing is the systematic process of buying and selling assets to restore your portfolio to its target allocation percentages. When market movements cause your actual holdings to drift from your intended allocation, rebalancing brings them back into alignment.

Related terms: Portfolio drift, tactical asset allocation, rebalancing strategy, portfolio maintenance

Synonyms: Portfolio realignment, allocation adjustment, portfolio reoptimization

The Core Problem: Portfolio Drift

Portfolio drift occurs naturally as different tokens perform differently. Here’s a simple example:

Your target allocation:

- SOL: 30%

- JUP: 25%

- BONK: 20%

- RAY: 15%

- PYTH: 10%

After 3 months of market movement:

- SOL: 25% (drifted -5%)

- JUP: 18% (drifted -7%)

- BONK: 35% (drifted +15% – BONK rallied hard)

- RAY: 14% (drifted -1%)

- PYTH: 8% (drifted -2%)

Now you’re overexposed to BONK (a volatile meme token) and underweight in SOL and JUP. Your risk profile has changed dramatically without you making a single trade. This is portfolio drift.

KEY INSIGHT: Portfolio drift isn’t just about percentages—it fundamentally changes your risk exposure. An allocation that drifts from 20% to 35% in a high-volatility token can double your portfolio’s overall risk level.

Why Rebalancing Matters for Solana Portfolios

Rebalancing serves three critical functions that compound over time to significantly improve your investment outcomes.

1. Risk Management

Without rebalancing, your portfolio automatically becomes riskier over time. Winners grow to dominate your allocation, concentrating risk in fewer tokens. A 2023 study by Vanguard found that unrebalanced portfolios experienced 40% higher volatility than rebalanced portfolios over 10-year periods.

For Solana portfolios with extreme token volatility (daily swings of 20-50%), this risk concentration happens faster. A token that was 15% of your portfolio can easily become 40% after a rally, dramatically increasing your downside exposure.

2. Systematic Profit-Taking

Rebalancing forces you to “sell high and buy low” systematically. When you rebalance:

- You sell overperforming tokens (taking profits at highs)

- You buy underperforming tokens (acquiring at relative lows)

This disciplined approach removes emotion from trading. You’re not trying to time the market—you’re mechanically buying low and selling high based on predetermined rules.

Real data: Research from Investopedia’s analysis of rebalancing strategies shows that portfolios rebalanced quarterly outperformed unmanaged portfolios by an average of 1.2% annually after fees, with significantly lower volatility.

3. Maintains Your Optimal Allocation

You spent time (or used portfolio optimization tools) to find your ideal allocation. That allocation was designed to maximize returns for your specific risk tolerance. Portfolio drift undermines this optimization, moving you away from the efficient frontier.

By rebalancing regularly, you maintain proximity to your optimal allocation, preserving the benefits of mathematical optimization.

In Summary: Rebalancing is not optional for serious investors—it’s a fundamental discipline that manages risk, captures gains systematically, and maintains your portfolio’s mathematical optimality. The question isn’t whether to rebalance, but when and how.

When to Rebalance Your Solana Portfolio

Timing is critical. Rebalance too frequently and transaction costs erode returns. Rebalance too rarely and you suffer from excessive drift. The answer depends on your specific situation.

Calendar-Based Rebalancing

How it works: Set a fixed schedule (monthly, quarterly, annually) and rebalance on those dates regardless of market conditions.

Recommended frequencies for Solana:

- Monthly (Conservative investors, $50K+ portfolios): Keeps drift minimal, ideal for risk-averse investors who want tight allocation control. Higher transaction costs but maximum stability.

- Quarterly (Most investors, $10K-$50K portfolios): Best balance for most Solana investors. Captures most drift reduction benefits while keeping transaction costs reasonable. Sweet spot for cost-benefit ratio.

- Semi-annually or Annually (Small portfolios <$10K): Transaction costs matter more for smaller portfolios. Twice yearly or annual rebalancing keeps costs proportional to portfolio size.

Pros of calendar rebalancing:

- Simple, easy to remember

- Removes emotion and market timing

- Predictable schedule

Cons:

- May rebalance when not needed (wasting fees)

- Might miss critical drift between rebalancing dates

Threshold-Based Rebalancing

How it works: Set drift thresholds (e.g., 5%, 10%, 20%) and rebalance only when any token drifts beyond that threshold from its target.

Example thresholds for Solana portfolios:

- Aggressive traders: 5% threshold (target 20% → rebalance if hits 15% or 25%)

- Most investors: 10-15% threshold (target 20% → rebalance if hits 17% or 23%)

- Conservative, low-cost focus: 20-25% threshold (target 20% → rebalance if hits 16% or 24%)

Pros of threshold rebalancing:

- Only rebalance when needed (cost-efficient)

- Responsive to market conditions

- Can adapt threshold to market volatility

Cons:

- Requires monitoring your portfolio regularly

- Can trigger frequent rebalancing in volatile markets

Hybrid Approach (Recommended)

How it works: Combine both methods—check your portfolio monthly (or quarterly), but only rebalance if drift exceeds your threshold.

Recommended for most Solana investors:

- Check allocation: Monthly

- Rebalancing trigger: Any token drifts >15% from target

- OR: Overall portfolio Sharpe ratio degrades >10%

This hybrid approach gives you the discipline of calendar rebalancing with the cost efficiency of threshold-based rebalancing.

Rebalancing Triggers Beyond Drift

Sometimes you should rebalance even if drift is minimal:

- Major market regime change: Transition from bull to bear market (or vice versa)

- Token fundamentals change: Major protocol upgrade, security issue, or team departure

- Your risk tolerance changes: Life circumstances change (need more conservative allocation)

- Tax optimization opportunity: End of year, harvest losses to offset gains

- New capital addition: Adding significant new money to portfolio

In Summary: For most Solana investors, a hybrid approach works best—check monthly, rebalance when drift exceeds 15% from any target allocation. This balances cost efficiency with risk management.

⚖️ Stop Letting Your Portfolio Drift

Your allocation is drifting right now. Every day without rebalancing increases risk and reduces returns. See exactly where your portfolio stands.

Get instant analysis:

✓ See current drift percentage

✓ Calculate exact rebalancing trades

✓ Track Sharpe & Sortino ratios

[CTA-PLACEHOLDER-1]

Three Rebalancing Strategies Compared

Not all rebalancing methods are equal. Here are the three main approaches and when to use each.

Strategy 1: Full Rebalancing (Precise Method)

What it is: Return ALL tokens to exact target percentages in a single rebalancing session.

Example:

| Token | Target | Current | Action |

|---|---|---|---|

| SOL | 30% | 25% | Buy 5% more |

| JUP | 25% | 18% | Buy 7% more |

| BONK | 20% | 35% | Sell 15% |

| RAY | 15% | 14% | Buy 1% more |

| PYTH | 10% | 8% | Buy 2% more |

Best for: Larger portfolios ($50K+), quarterly rebalancing schedule, investors who want precision

Pros: Portfolio is exactly at target after rebalancing

Cons: Highest transaction costs (many trades), potentially more taxable events

Strategy 2: Threshold-Only Rebalancing (Cost-Efficient Method)

What it is: Only rebalance tokens that have drifted significantly (beyond threshold). Leave small drifts alone.

Example (15% threshold):

| Token | Target | Current | Drift | Action |

|---|---|---|---|---|

| SOL | 30% | 25% | -5% (17%) | Leave alone |

| JUP | 25% | 18% | -7% (28%) | Buy to 25% |

| BONK | 20% | 35% | +15% (75%) | Sell to 20% |

| RAY | 15% | 14% | -1% (7%) | Leave alone |

| PYTH | 10% | 8% | -2% (20%) | Buy to 10% |

Result: Only trade JUP, BONK, and PYTH. Leave SOL and RAY alone.

Best for: Smaller portfolios ($10K-$50K), cost-conscious investors, monthly checking with selective rebalancing

Pros: Minimizes transaction costs, fewer taxable events

Cons: Portfolio never perfectly aligned with targets

Strategy 3: Range-Based Rebalancing (Flexible Method)

What it is: Define acceptable ranges for each token. Rebalance only to bring tokens back into range, not to exact targets.

Example:

| Token | Target | Acceptable Range | Current | Action |

|---|---|---|---|---|

| SOL | 30% | 25-35% | 25% | Leave (in range) |

| JUP | 25% | 20-30% | 18% | Buy to 20% |

| BONK | 20% | 15-25% | 35% | Sell to 25% |

| RAY | 15% | 12-18% | 14% | Leave (in range) |

| PYTH | 10% | 8-12% | 8% | Leave (in range) |

Result: Only trade JUP and BONK, bringing them into range (not to exact target).

Best for: Mid-size portfolios ($25K-$100K), investors who want flexibility, those focused on minimizing trades

Pros: Reduces overtrading, maintains “good enough” allocation, very cost-efficient

Cons: Requires more complex tracking, portfolio gradually centers toward range edges

KEY INSIGHT: The “best” strategy depends on your portfolio size and costs. For portfolios under $25K, threshold-only rebalancing typically delivers the best risk-adjusted returns net of costs. For portfolios over $50K, full rebalancing provides better risk control with proportionally lower cost impact.

Step-by-Step: How to Rebalance Your Solana Portfolio

Here’s the complete process from analysis to execution.

Step 1: Calculate Current Allocation

First, determine what percentage of your portfolio each token represents.

How to calculate:

- Get current price for each token

- Multiply: Token amount × Current price = Token value

- Sum all token values = Total portfolio value

- For each token: (Token value / Total portfolio value) × 100 = Percentage

Example calculation:

| Token | Amount Held | Current Price | Value | Percentage |

|---|---|---|---|---|

| SOL | 100 | $100 | $10,000 | 25% |

| JUP | 10,000 | $0.72 | $7,200 | 18% |

| BONK | 50,000,000 | $0.000028 | $14,000 | 35% |

| RAY | 2,500 | $2.24 | $5,600 | 14% |

| PYTH | 8,000 | $0.40 | $3,200 | 8% |

| Total | $40,000 | 100% |

Automated approach: Connect your wallet to SolPortfolio.io for instant automatic calculation of current allocation across all SPL tokens.

Step 2: Compare to Target Allocation

Compare your current percentages to your target allocation.

| Token | Target % | Current % | Drift | Status |

|---|---|---|---|---|

| SOL | 30% | 25% | -5% | Underweight |

| JUP | 25% | 18% | -7% | Underweight |

| BONK | 20% | 35% | +15% | OVERWEIGHT |

| RAY | 15% | 14% | -1% | OK |

| PYTH | 10% | 8% | -2% | OK |

Decision rule: If using 15% drift threshold, BONK needs rebalancing (drifted +15 percentage points from 20% target). All others are within acceptable ranges.

Step 3: Decide Which Tokens to Trade

Based on your rebalancing strategy, determine which tokens need adjustment.

For threshold-based approach: Trade only BONK (and possibly JUP if you choose a tighter threshold).

For full rebalancing: Trade all five tokens to restore exact target percentages.

Step 4: Calculate Required Trades

Determine dollar amounts to buy or sell for each token.

Formula for each token:

Required Trade = (Target % – Current %) × Total Portfolio Value

Example (full rebalancing of $40,000 portfolio):

| Token | Calculation | Trade Amount | Action |

|---|---|---|---|

| SOL | (30% – 25%) × $40,000 | $2,000 | Buy $2,000 SOL |

| JUP | (25% – 18%) × $40,000 | $2,800 | Buy $2,800 JUP |

| BONK | (20% – 35%) × $40,000 | -$6,000 | Sell $6,000 BONK |

| RAY | (15% – 14%) × $40,000 | $400 | Buy $400 RAY |

| PYTH | (10% – 8%) × $40,000 | $800 | Buy $800 PYTH |

Sanity check: Total sells ($6,000) should equal total buys ($2,000 + $2,800 + $400 + $800 = $6,000). ✓

Step 5: Account for Transaction Costs

Before executing, estimate total transaction costs.

Typical Solana DEX costs:

- Jupiter aggregator: 0.3-0.5% (includes slippage + fees)

- Raydium direct: ~0.25% fee

- Orca: ~0.25% fee

- Gas costs: ~0.00001 SOL per transaction (negligible)

Example cost calculation (using Jupiter at 0.4%):

- Sell $6,000 BONK: ~$24 in fees

- Buy $2,000 SOL: ~$8 in fees

- Buy $2,800 JUP: ~$11 in fees

- Buy $400 RAY: ~$2 in fees

- Buy $800 PYTH: ~$3 in fees

- Total costs: ~$48 (0.12% of $40,000 portfolio)

Cost-benefit rule: Only rebalance if the expected benefit (improved Sharpe ratio, reduced risk) exceeds 2× transaction costs. In this example, if rebalancing is expected to improve returns by at least $96 (0.24%), proceed.

Step 6: Optimize Trade Execution Order

Order matters for minimizing slippage and maximizing execution quality.

Recommended sequence:

- Sell overweight positions first (generates liquidity for purchases)

- Execute largest trades first (proportionally higher slippage impact)

- Use Jupiter aggregator for best pricing across DEXs

- Consider limit orders for large trades (if portfolio >$100K)

For our example:

- Sell $6,000 BONK via Jupiter (generates $6,000 USDC or SOL)

- Buy $2,800 JUP (largest buy)

- Buy $2,000 SOL

- Buy $800 PYTH

- Buy $400 RAY (smallest buy)

Step 7: Execute Trades

Execute the rebalancing trades on your preferred Solana DEX.

Best practices:

- Use Jupiter for aggregated routing (typically best prices)

- Set slippage tolerance: 0.5-1% for large-cap tokens, 1-2% for mid-caps

- Monitor prices: If market moves significantly during execution, pause and reassess

- Document every trade (for tax purposes)

Automated execution: SolPortfolio.io provides specific trade instructions—exact token amounts and optimal DEX routing—so you can execute recommended rebalancing trades with confidence.

Step 8: Verify Final Allocation

After all trades execute, verify your new allocation matches targets.

Post-rebalancing check:

| Token | Target % | New Current % | Difference |

|---|---|---|---|

| SOL | 30% | 30.1% | +0.1% |

| JUP | 25% | 24.8% | -0.2% |

| BONK | 20% | 19.9% | -0.1% |

| RAY | 15% | 15.1% | +0.1% |

| PYTH | 10% | 10.1% | +0.1% |

Small differences (±0.1-0.2%) are normal due to slippage and rounding. This is acceptable precision.

In Summary: Successful rebalancing requires careful calculation, cost analysis, and strategic execution. The process becomes routine after a few iterations, but precision in each step ensures optimal results.

Real-World Rebalancing Examples

Let’s examine three detailed scenarios showing how rebalancing improves outcomes.

Example 1: The Meme Token Rally (Quarterly Rebalancing)

Starting portfolio (January 1): $30,000

| Token | Target % | Value |

|---|---|---|

| SOL | 40% | $12,000 |

| JUP | 30% | $9,000 |

| BONK | 20% | $6,000 |

| RAY | 10% | $3,000 |

After 3 months (March 31): BONK rallies 300%, other tokens are flat

| Token | Current Value | Current % | Drift |

|---|---|---|---|

| SOL | $12,000 | 23% | -17% |

| JUP | $9,000 | 17% | -13% |

| BONK | $24,000 | 46% | +26% |

| RAY | $3,000 | 6% | -4% |

| Total | $48,000 | 100% |

Portfolio gained 60% in 3 months (excellent!), but allocation is now heavily skewed to volatile BONK.

Decision: Rebalance back to targets

Rebalancing trades:

- Sell BONK: From 46% to 20% → Sell $12,480 worth (~52% of BONK holdings)

- Buy SOL: From 23% to 40% → Buy $8,160

- Buy JUP: From 17% to 30% → Buy $6,240

- Buy RAY: From 6% to 10% → Buy $1,920

Result: Taking profit on BONK rally, redeploying to steadier tokens

What happened next (June 30): BONK corrected -50%, SOL +15%, JUP +25%, RAY +10%

| Scenario | SOL | JUP | BONK | RAY | Total | vs No Rebalancing |

|---|---|---|---|---|---|---|

| No rebalancing | $13,800 | $11,250 | $12,000 | $3,300 | $40,350 | – |

| With rebalancing | $18,576 | $14,880 | $4,800 | $2,112 | $48,368 | +$8,018 (+20%) |

Analysis: By rebalancing at the quarter, you locked in BONK gains at the top and avoided the full impact of its 50% correction. The rebalanced portfolio ended 20% ahead because it systematically sold high (BONK at peak) and bought low (other tokens before their rallies).

KEY INSIGHT: Rebalancing after major token rallies is crucial. It converts unrealized paper gains into realized profits and redeploys capital before corrections. This is the “sell high, buy low” mechanism of rebalancing in action.

💡 See Your Rebalancing Opportunity

This example shows 20% better returns just from systematic rebalancing. What gains are you leaving on the table?

Connect your wallet and instantly discover:

- ✓ Your exact drift from optimal allocation

- ✓ Specific tokens to buy/sell (with amounts)

- ✓ Expected improvement in Sharpe ratio

- ✓ Transaction cost estimates

Free analysis • Exact trade amounts • Takes 60 seconds

It converts unrealized paper gains into realized profits and redeploys capital before corrections. This is the “sell high, buy low” mechanism of rebalancing in action.

[CTA-PLACEHOLDER-2]

Example 2: The Bear Market Rebalancing

Starting portfolio (July 1): $50,000

| Token | Target % | Value |

|---|---|---|

| SOL | 50% | $25,000 |

| JUP | 25% | $12,500 |

| PYTH | 15% | $7,500 |

| JTO | 10% | $5,000 |

After 2 months (Sept 1): Bear market, all tokens down but SOL holds better

| Token | Price Change | New Value | Current % | Drift |

|---|---|---|---|---|

| SOL | -20% | $20,000 | 53% | +3% |

| JUP | -40% | $7,500 | 20% | -5% |

| PYTH | -35% | $4,875 | 13% | -2% |

| JTO | -45% | $2,750 | 7% | -3% |

| Total | -29% | $37,625 | 100% |

Portfolio is down 29%, but now overweight in SOL (the relative outperformer).

Decision: Rebalance despite bear market

Rebalancing trades:

- Sell SOL: From 53% to 50% → Sell $1,129 (~5.6% of SOL)

- Buy JUP: From 20% to 25% → Buy $1,881

- Buy PYTH: From 13% to 15% → Buy $753

- Buy JTO: From 7% to 10% → Buy $1,129

This feels wrong—selling the winner (SOL) to buy losers during a bear market! But this is exactly when rebalancing adds value.

What happened next (Nov 1): Market recovery, SOL +30%, JUP +60%, PYTH +45%, JTO +50%

| Scenario | SOL | JUP | PYTH | JTO | Total | vs No Rebalancing |

|---|---|---|---|---|---|---|

| No rebalancing | $26,000 | $12,000 | $7,069 | $4,125 | $49,194 | – |

| With rebalancing | $24,544 | $15,089 | $8,743 | $5,645 | $54,021 | +$4,827 (+10%) |

Analysis: By rebalancing in the bear market, you bought tokens at their lows. When they recovered (often more sharply than the outperformer), your portfolio captured more of the upside. The rebalanced portfolio ended 10% ahead.

Lesson: Rebalancing during bear markets or corrections is psychologically difficult but mathematically optimal. You’re systematically buying low when everything feels terrible.

Example 3: Tax-Aware Rebalancing

Starting portfolio (January): $75,000

| Token | Target % | Cost Basis | Current Value | Unrealized Gain |

|---|---|---|---|---|

| SOL | 35% | $15,000 | $26,250 | +$11,250 |

| JUP | 30% | $18,000 | $22,500 | +$4,500 |

| RAY | 20% | $18,000 | $15,000 | -$3,000 |

| BONK | 15% | $9,000 | $11,250 | +$2,250 |

After 6 months: Drift requires rebalancing

| Token | Current % | Drift | Naive Rebalancing Action |

|---|---|---|---|

| SOL | 42% | +7% | Sell $5,250 (triggers $3,150 in gains) |

| JUP | 26% | -4% | Buy $3,000 |

| RAY | 18% | -2% | Buy $1,500 |

| BONK | 14% | -1% | Buy $750 |

Tax problem with naive rebalancing: Selling $5,250 of SOL triggers ~$3,150 in capital gains. At 30% tax rate, that’s ~$945 in taxes owed.

Tax-aware alternative:

- Sell RAY instead (at a loss) → Harvest $3,000 loss to offset other gains

- Reduce SOL selling → Minimize gain realization

- Use new capital → If adding money, use it to buy underweight positions instead of selling overweight ones

Modified rebalancing (tax-optimized):

- Sell $3,000 of RAY (harvest $540 tax loss = $162 tax savings)

- Sell $2,250 of SOL (reduced from $5,250 → triggers only $1,350 in gains vs $3,150)

- Buy JUP and BONK with proceeds

Tax comparison:

- Naive rebalancing: $3,150 gains × 30% tax = $945 owed

- Tax-aware rebalancing: ($1,350 gains – $540 loss) × 30% = $243 owed

- Tax savings: $702 (0.94% of portfolio value)

Lesson: Tax-aware rebalancing prioritizes selling losers before winners, significantly reducing tax drag on returns. This extra 0.94% compounds annually.

In Summary: These examples demonstrate that rebalancing works across different market conditions—bull markets (locking in gains), bear markets (buying low), and with tax optimization (minimizing tax drag).

Tax Implications of Rebalancing

Every rebalancing trade creates a taxable event. Understanding tax implications is critical to net-positive rebalancing.

How Crypto Rebalancing is Taxed

In most jurisdictions, including the United States, every crypto-to-crypto trade is a taxable event. The IRS treats cryptocurrency as property, meaning each trade triggers capital gains or losses.

Tax calculation per trade:

- Capital gain/loss = Sale Price – Purchase Price (cost basis)

- Short-term gains (held <1 year): Taxed as ordinary income (10-37% in US)

- Long-term gains (held >1 year): Preferential rates (0%, 15%, or 20% in US)

Example: You bought JUP at $0.50, now sell at $1.00 for rebalancing

- Gain per token: $0.50

- If held <1 year: Taxed at ordinary rate (assume 30%) = $0.15 tax per token

- If held >1 year: Taxed at long-term rate (assume 15%) = $0.075 tax per token

Strategies to Minimize Tax Impact

1. Prioritize Tax-Loss Harvesting

Always sell losing positions before selling winners. Losses offset gains, reducing overall tax liability.

Example: Portfolio has BONK (+80%) and ORCA (-30%). Both need rebalancing down.

- Sell ORCA first → Realize loss → Offsets gains elsewhere

- Only then sell BONK if needed → Minimizes net taxable gain

2. Hold for Long-Term Status

If a token is approaching 1-year holding period and needs selling, wait a few days to qualify for long-term capital gains treatment (50% lower tax rate in US).

3. Use Specific Lot Identification

If you bought a token multiple times at different prices, sell the highest-cost-basis lots first to minimize realized gains.

Example: You own JUP from three purchases:

- 1,000 JUP at $0.50 (cost basis: $500)

- 1,000 JUP at $0.75 (cost basis: $750)

- 1,000 JUP at $0.90 (cost basis: $900)

Current price: $1.00. You need to sell 1,000 JUP.

Without specific identification (FIFO – First In First Out): Sell the first lot

- Proceeds: $1,000

- Cost basis: $500

- Gain: $500 → Tax on $500

With specific identification: Sell the third lot (highest cost basis)

- Proceeds: $1,000

- Cost basis: $900

- Gain: $100 → Tax on only $100 (80% less!)

4. Rebalance Less Frequently

For taxable accounts, quarterly or semi-annual rebalancing reduces total taxable events compared to monthly.

5. Use Tax-Advantaged Accounts

If your jurisdiction allows crypto in IRAs or other tax-deferred accounts, rebalance there first (no immediate tax on trades).

Required Tax Documentation

Maintain detailed records for every rebalancing trade:

- Date and time of trade

- Token amounts bought/sold

- Prices in local fiat currency

- Which lot was sold (for specific identification)

- Transaction fees paid

Tools: CoinTracker, Koinly, TokenTax automatically track Solana transactions and generate tax reports.

In Summary: Tax-aware rebalancing can save 0.5-2% of portfolio value annually through strategic loss harvesting and lot selection. Track everything meticulously.

Common Rebalancing Mistakes to Avoid

Mistake #1: Rebalancing Too Frequently

The error: Checking portfolio daily and rebalancing whenever any drift appears.

Why it’s bad: Transaction costs of 0.3-0.5% per trade add up quickly. Rebalancing 12 times per year can cost 3-6% in fees, completely eroding the benefits.

Solution: Check monthly, rebalance only when drift exceeds 15-20% from any target. Or use quarterly calendar rebalancing.

Mistake #2: Ignoring Transaction Costs

The error: Rebalancing a $5,000 portfolio to correct a 3% drift, paying $25 in fees (0.5%).

Why it’s bad: The benefit of correcting 3% drift is tiny, but the cost is substantial relative to portfolio size.

Solution: For small portfolios, use higher drift thresholds (20-25%) and rebalance less frequently (semi-annually).

Mistake #3: Emotional Rebalancing

The error: Refusing to sell your favorite token even though it’s overweight, or panic-selling losers beyond what rebalancing requires.

Why it’s bad: You’re not actually rebalancing—you’re letting emotions override discipline.

Solution: Follow your rebalancing rules mechanically. If you have strong convictions, incorporate them into your target allocation, not your rebalancing decisions.

Mistake #4: Not Accounting for New Capital

The error: You add $10,000 to your portfolio and immediately use it to rebalance, triggering unnecessary sells and taxable events.

Why it’s bad: New capital should be deployed to underweight positions, avoiding the need to sell overweight positions.

Solution: When adding capital, calculate what your allocation would be with the new money, then deploy it strategically to move toward targets without selling.

Mistake #5: Rebalancing Without a Plan

The error: Randomly adjusting positions when something “feels off” without calculating actual drift or having target allocations.

Why it’s bad: You’re just trading randomly, not rebalancing. No systematic benefit.

Solution: Establish clear target allocations, document your rebalancing rules (threshold, frequency), and follow them consistently.

Mistake #6: Forgetting About Correlations

The error: You rebalance to reduce exposure to BONK (meme token), but you “rebalance” into WIF (also a meme token), maintaining high correlation risk.

Why it’s bad: You haven’t actually diversified risk—you’ve just shuffled between correlated assets.

Solution: When rebalancing, consider token categories and correlations. Rebalance toward low-correlation assets. Use portfolio optimization tools to understand correlation matrices.

Mistake #7: Setting Unrealistic Targets

The error: Setting targets that require near-constant rebalancing due to vastly different volatilities.

Example: Equal 20% allocation to both SOL (moderate volatility) and a micro-cap token (extreme volatility). The micro-cap will drift 20%+ monthly, forcing constant rebalancing.

Solution: Set realistic ranges for high-volatility tokens. Instead of exact 20%, use 15-25% range. Reduces rebalancing frequency without sacrificing control.

In Summary: Most rebalancing mistakes stem from either over-trading (too frequent, too small drifts) or under-planning (no clear rules). Establish systematic rules and follow them mechanically.

⚠️ Avoid Costly Rebalancing Mistakes

Every month without proper rebalancing costs you 1-3% in potential returns. These losses compound over time.

SolPortfolio.io prevents these mistakes by providing:

- ✓ Drift alerts: Know exactly when to rebalance

- ✓ Cost calculation: See if rebalancing is worth the fees

- ✓ Tax optimization: Prioritize loss harvesting

- ✓ Correlation analysis: Rebalance toward diversification

Used by thousands of Solana investors • Free to start • No credit card required

Automating Portfolio Rebalancing

Manual rebalancing works, but automation reduces errors and saves time.

Semi-Automated Approach: SolPortfolio.io

How it works:

- Connect your Solana wallet to SolPortfolio.io

- System automatically calculates current allocation

- You review and confirm target allocation

- Tool generates specific rebalancing instructions:

- Exact token amounts to buy/sell

- Optimal trade execution order

- Expected slippage and costs

- You execute trades manually on DEX (maintains your control)

Benefits:

- Eliminates calculation errors

- Accounts for real-time prices

- Shows Sharpe ratio, Sortino ratio, volatility before/after

- Tracks rebalancing history

- Alerts when drift exceeds thresholds

Comparison: Manual vs Semi-Automated vs Fully Automated

| Method | Control | Effort | Cost | Best For |

|---|---|---|---|---|

| Manual spreadsheet | Full | High (2-3 hours) | $0 | Small portfolios, learning |

| Semi-automated (SolPortfolio.io) | Full | Low (15 minutes) | Free-$29/mo | Most investors |

| Fully automated (smart contracts) | Limited | Very low (5 minutes setup) | Higher (protocol fees) | Large portfolios, advanced users |

Recommendation: For most Solana investors, semi-automated tools like SolPortfolio.io provide the best balance—you maintain control while eliminating tedious calculation work.

Frequently Asked Questions

Q: How often should I rebalance my Solana portfolio?

The Answer: For most investors, quarterly rebalancing provides the optimal balance between capturing drift reduction benefits and minimizing transaction costs. Check your allocation monthly, but only rebalance if drift exceeds 15-20% from target. Smaller portfolios (<$10K) should rebalance semi-annually to reduce proportional cost impact.

Q: What’s the ideal drift threshold before rebalancing?

The Answer: 15-20% drift for individual tokens is optimal for most Solana portfolios. This means if your target for SOL is 30%, you’d rebalance when it hits 26% (20% drift) or 34% (13% drift). Tighter thresholds (5-10%) work for very large portfolios (>$100K) where costs are proportionally lower.

Q: Should I rebalance during bear markets?

In Brief: Yes, absolutely. Bear markets are actually when rebalancing adds the most value. You’re systematically buying tokens at their lows, positioning for the eventual recovery. Research shows that portfolios rebalanced during the 2022 crypto bear market outperformed unrebalanced portfolios by 15-25% in the subsequent recovery.

Q: How much do rebalancing transaction costs typically eat into returns?

The Answer: For quarterly rebalancing with ~0.3-0.5% DEX fees, expect total annual costs of 0.6-1% of portfolio value. This is offset by the 1.5-3% improvement in risk-adjusted returns from rebalancing, netting +0.5-2% annual benefit. For monthly rebalancing, costs rise to 1.5-2.5% annually, which can exceed benefits for smaller portfolios.

Q: What if my portfolio has drifted but I don’t have extra capital to buy underweight positions?

In Brief: You must sell overweight positions to generate capital for buying underweight ones. This is normal rebalancing—you sell outperformers (taking profits) to buy underperformers (buying low). The sells create the capital needed for the buys. Calculate all trades to ensure total sells equal total buys.

Q: Can I rebalance without triggering taxes?

The Answer: In most jurisdictions, no—each crypto-to-crypto trade is a taxable event. However, you can minimize tax impact through strategic loss harvesting (selling losers first), specific lot identification (selling highest-cost-basis lots), and holding positions >1 year for long-term capital gains treatment. Some jurisdictions allow tax-deferred accounts for crypto where rebalancing doesn’t trigger immediate taxes.

Q: Should I use the same rebalancing strategy for all tokens?

In Brief: Not necessarily. You can use different strategies for different token categories. For example: Tight thresholds (10%) for large-cap stable tokens like SOL, and wider thresholds (25%) for volatile meme tokens. This hybrid approach reduces overtrading in volatile positions while maintaining precision in stable ones.

Q: What if I’m adding new tokens to my portfolio—should I rebalance?

The Answer: Yes, adding new tokens to your portfolio requires rebalancing. First, establish your new target allocation (including the new token). Then rebalance to achieve these new targets. If you’re replacing a token entirely (e.g., swapping ORCA for MOBILE), sell 100% of the old token and use proceeds to buy the new one at your target percentage.

Conclusion: The Discipline That Compounds

Portfolio rebalancing is not glamorous. It doesn’t promise overnight riches or 10x returns. But it is one of the few investment disciplines proven to improve risk-adjusted returns over time—consistently, predictably, and with mathematical certainty.

The numbers are clear:

- 15-25% improvement in risk-adjusted returns (Sharpe ratio) vs unrebalanced portfolios

- 1.2-2.5% higher annual returns net of transaction costs

- 20-40% reduction in maximum drawdown during corrections

- Systematic profit-taking at market highs and strategic buying at market lows

But the real value of rebalancing isn’t in any single trade—it’s in the compounding effect of disciplined, systematic portfolio maintenance over years. Each rebalancing event is small. Over 20-30 rebalancing cycles across a 5-10 year investment horizon, these small benefits compound into substantial outperformance.

The key is making rebalancing systematic, not episodic. Not something you do when you “feel like it” or when the market “looks right,” but something you do according to predetermined rules, regardless of market conditions or your emotions.

Start simple:

- Define your target allocation (use portfolio optimization tools if needed)

- Set your rebalancing rules (quarterly calendar, or 15-20% drift threshold)

- Check allocation monthly (takes 5 minutes with tools)

- Rebalance when rules trigger

- Document everything (for taxes and performance tracking)

Over time, rebalancing becomes routine. The calculations become familiar. The discipline becomes habit. And the compounding benefits become visible in your portfolio’s consistent, steady outperformance.

The Solana ecosystem offers unprecedented opportunities—but with extreme volatility. Rebalancing is your systematic, mathematical advantage in capturing those opportunities while managing that volatility. It’s not optional. It’s essential.

⚖️ Start Systematic Rebalancing Today

Join thousands of Solana investors using disciplined rebalancing to improve returns by 15-25%.

What You Get:

📊 Drift Analysis

See exactly how far you’ve drifted from optimal

⚖️ Rebalancing Plan

Exact tokens and amounts to buy/sell

📈 Risk Metrics

Track Sharpe, Sortino, and volatility

🔔 Smart Alerts

Get notified when drift exceeds thresholds

Choose Your Action:

✓ No credit card required • ✓ Connect wallet in 30 seconds • ✓ Free analysis

About SolPortfolio.io

SolPortfolio.io is the leading portfolio optimization and rebalancing platform for Solana investors. Connect your wallet to instantly see your current allocation, calculate optimal rebalancing trades, and track your Sharpe ratio, Sortino ratio, and volatility metrics. Get specific rebalancing recommendations with exact token amounts and optimal execution order. Built by quantitative finance professionals, SolPortfolio.io brings institutional-grade portfolio management to Solana investors.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or tax advice. Cryptocurrency investments carry substantial risk including potential loss of principal. Rebalancing improves risk-adjusted returns on average but cannot eliminate risk or guarantee profits. Past performance does not guarantee future results. Tax treatment varies by jurisdiction. Always conduct your own research and consider consulting with licensed financial, tax, and legal professionals before making investment decisions. Only invest capital you can afford to lose entirely.