Solana Risk Management: How to Protect Your Portfolio (2026)

Solana Risk Management: How to Protect Your Portfolio (2026)

You’ve optimized your Solana portfolio. You’re rebalancing regularly. Your allocation looks perfect on paper. But then a token crashes 60% overnight. Or a protocol you’re using gets exploited. Or market-wide correlation sends everything down together. Suddenly, your carefully constructed portfolio is down 40% in a week.

Portfolio optimization and rebalancing improve returns—but they don’t protect against catastrophic losses. That’s where risk management comes in. For Solana investors facing extreme volatility (daily swings of 20-50%), systematic risk management isn’t optional—it’s the difference between surviving market crashes and losing everything.

This comprehensive guide shows you exactly how to identify, measure, and mitigate the five critical risks facing every Solana portfolio: volatility risk, concentration risk, correlation risk, protocol risk, and liquidity risk. You’ll learn practical strategies used by professional traders to protect capital while maintaining upside potential.

What Is Portfolio Risk Management?

DEFINITION: Portfolio risk management is the systematic process of identifying, measuring, and mitigating potential losses in your investment portfolio. For crypto investors, this means protecting against downside risk while maintaining exposure to upside potential through position sizing, diversification, and active monitoring.

Related terms: Risk assessment, downside protection, capital preservation, risk-adjusted returns, value at risk (VaR)

Synonyms: Portfolio protection, risk mitigation, capital protection, defensive investing

Why Risk Management Matters More for Solana

Solana tokens exhibit significantly higher volatility than traditional assets:

- Traditional stocks: Average daily volatility ~1-2%

- Bitcoin/Ethereum: Average daily volatility ~3-5%

- Solana ecosystem tokens: Average daily volatility ~8-15%

- New Solana tokens: Daily volatility can exceed 50%

This extreme volatility means a Solana portfolio without proper risk management can experience drawdowns of 70-90% during bear markets, even with good token selection. Proper risk management reduces maximum drawdown to 30-50% while maintaining most of the upside.

KEY INSIGHT: Risk management isn’t about avoiding risk entirely—it’s about taking calculated risks with defined downside limits. The goal is asymmetric returns: limited downside with unlimited upside.

Understanding the Five Critical Risks

Every Solana portfolio faces five distinct categories of risk. Understanding each is essential for comprehensive protection.

1. Volatility Risk

What it is: The risk of price fluctuations causing temporary or permanent capital loss.

How to measure: Standard deviation of daily returns. Higher standard deviation = higher volatility = higher risk.

Example: Token A averages 10% daily volatility. This means roughly 68% of days will see price changes within ±10%, but 32% of days will see larger moves. Extreme days (5% probability) can see 20%+ moves.

Why it matters: High volatility increases the probability of large drawdowns and can force you to sell at the worst times due to emotional stress.

2. Concentration Risk

What it is: The risk of having too much capital in a single token, sector, or position.

How to measure: Percentage allocation to any single token. Professional risk management limits single positions to 10-20% of portfolio.

Example: Portfolio with 60% in one token. If that token drops 50%, total portfolio drops 30%—regardless of how other tokens perform.

Why it matters: Concentration creates asymmetric downside risk. You can only lose 100% on a position, but concentrated positions mean one token’s failure destroys the entire portfolio.

3. Correlation Risk

What it is: The risk that multiple positions move in the same direction simultaneously, eliminating diversification benefits.

How to measure: Correlation coefficient between token pairs (-1 to +1). High positive correlation (>0.7) means tokens move together.

Example: Portfolio holding 5 different DeFi governance tokens (JUP, RAY, ORCA, MNGO, DRIFT). All are positively correlated (0.8+), so when DeFi sentiment turns negative, all drop together. You think you’re diversified, but you’re not.

Why it matters: Correlation risk is the silent killer of diversification. During crashes, previously uncorrelated assets often become highly correlated, causing “everything down” scenarios.

The solution: Modern Portfolio Theory (Markowitz optimization) explicitly accounts for correlations when building portfolios. Tools like SolPortfolio.io calculate correlation matrices and recommend truly diversified allocations that reduce correlated risk.

4. Protocol Risk

What it is: The risk that a DeFi protocol you’re using gets hacked, exploited, or fails.

Key statistics: According to blockchain security firm CertiK, DeFi protocols lost over $1.8 billion to hacks and exploits in 2023 alone. Solana DeFi has seen multiple major incidents including the Wormhole bridge hack ($325M) and Mango Markets exploit ($110M).

Why it matters: Unlike centralized exchanges where you might recover funds, DeFi exploits often result in permanent loss. Once tokens are drained, they’re gone.

5. Liquidity Risk

What it is: The risk that you cannot sell a position quickly without significant price impact.

How to measure: Daily trading volume relative to your position size. Rule of thumb: your position should not exceed 10% of daily volume.

Example: You hold $50,000 of a token with $200,000 daily volume. Your position is 25% of daily volume. When you try to sell, slippage will be 5-10% or more. You’re effectively trapped.

Why it matters: Illiquid positions become “forced holders” during crashes. You watch your portfolio collapse but can’t exit without massive losses from slippage.

In Summary: These five risks compound during market stress. A concentrated, illiquid, highly correlated portfolio in a volatile market can experience 80-90% drawdowns. Proper risk management addresses each risk category systematically.

Measuring Your Portfolio’s Risk Profile

Before you can manage risk, you must measure it. Here are the key metrics every Solana investor should track.

Portfolio Volatility (Standard Deviation)

What it measures: How much your total portfolio value fluctuates day-to-day.

How to calculate:

- Track daily portfolio value for 30-90 days

- Calculate daily returns: (Today’s Value – Yesterday’s Value) / Yesterday’s Value

- Calculate standard deviation of daily returns

- Annualize by multiplying by √365

Interpretation:

- Low risk: 30-50% annualized volatility

- Moderate risk: 50-100% annualized volatility

- High risk: 100-150% annualized volatility

- Extreme risk: >150% annualized volatility

Automated approach: Connect your wallet to SolPortfolio.io for automatic volatility calculation and historical tracking.

📊 Know Your Risk Profile

Understanding your portfolio’s risk is the first step to protecting it. Get instant risk analytics for your Solana holdings.

Free Risk Analysis:

✓ Volatility & Sharpe ratio calculated instantly

✓ Correlation matrix analysis

✓ Maximum drawdown tracking

Maximum Drawdown (MDD)

What it measures: The largest peak-to-trough decline your portfolio has experienced.

Formula: MDD = (Trough Value – Peak Value) / Peak Value × 100

Example:

- Portfolio peak: $100,000 (January 1)

- Portfolio trough: $45,000 (March 15)

- MDD = ($45,000 – $100,000) / $100,000 = -55%

Why it matters: MDD tells you the worst-case historical loss. Psychologically, most investors cannot tolerate MDD >50% without panic selling. If your MDD exceeds your risk tolerance, your portfolio is too aggressive.

Value at Risk (VaR)

What it measures: The maximum expected loss over a specific time period at a given confidence level.

Example: “1-day VaR at 95% confidence = 8%” means there’s a 95% probability your portfolio won’t lose more than 8% in any given day. Conversely, there’s a 5% chance (roughly once per month) you’ll lose more than 8% in a single day.

Practical use: VaR helps you set realistic expectations. If your 1-day VaR is 15%, you should expect occasional 15%+ down days. If that would cause panic, reduce risk.

Sharpe Ratio

What it measures: Risk-adjusted returns. How much return you’re getting per unit of risk taken.

Formula: Sharpe Ratio = (Portfolio Return – Risk-Free Rate) / Portfolio Volatility

Interpretation:

- Sharpe < 0.5: Poor risk-adjusted returns

- Sharpe 0.5-1.0: Acceptable

- Sharpe 1.0-2.0: Good

- Sharpe > 2.0: Excellent (rare in crypto)

Why it matters: A portfolio returning 100% with 150% volatility (Sharpe 0.67) is worse than a portfolio returning 60% with 50% volatility (Sharpe 1.2). The second portfolio delivers better risk-adjusted returns.

Sortino Ratio

What it measures: Like Sharpe ratio, but only penalizes downside volatility, not upside.

Why it matters: Sharpe ratio treats upside and downside volatility equally. But investors only care about downside risk. Sortino ratio gives a more accurate picture by only measuring harmful volatility.

Interpretation: Higher Sortino = better downside-protected returns. Professional portfolios target Sortino > 1.0.

Position Sizing: The Kelly Criterion for Solana

Position sizing determines how much capital to allocate to each token. Too large = excessive risk. Too small = insufficient returns.

The Kelly Criterion

What it is: A mathematical formula for optimal position sizing that maximizes long-term compound growth while managing risk.

Formula: Kelly % = (Win Probability × Average Win) – (Loss Probability × Average Loss) / Average Win

Example:

- Token has 60% probability of 20% gain, 40% probability of 10% loss

- Kelly % = (0.6 × 0.2) – (0.4 × 0.1) / 0.2 = 40%

- Optimal position size = 40% of portfolio

Practical Kelly for Crypto: Full Kelly is too aggressive for crypto’s extreme volatility. Most professionals use “Half Kelly” (divide Kelly % by 2) for safety margin.

Modified Kelly for Solana Portfolios:

- High confidence tokens (SOL, established DeFi): 10-20% position (Half Kelly)

- Medium confidence (newer protocols): 5-10% position (Quarter Kelly)

- Speculative positions: 2-5% position maximum

- Never exceed 25% in any single position regardless of Kelly calculation

Practical Position Sizing Rules

Conservative approach (beginners, <$25K portfolios):

- Largest position: 20% maximum

- Top 3 positions: 50% maximum combined

- Minimum 5 different tokens

- No speculative positions >5%

Moderate approach (experienced, $25K-$100K):

- Largest position: 25% maximum

- Top 3 positions: 60% maximum combined

- Minimum 6-8 different tokens

- Speculative positions: 10% combined maximum

Aggressive approach (professional, >$100K):

- Largest position: 30% maximum

- Top 3 positions: 70% maximum combined

- 8-12 different tokens

- Speculative positions: 15% combined maximum

KEY INSIGHT: Position sizing is the most important risk management tool. Even with perfect token selection, oversized positions create catastrophic risk. A 50% position that drops 80% = 40% total portfolio loss. Proper position sizing limits single-token disasters to manageable losses.

Diversification: Building Uncorrelated Positions

Holding 10 different tokens doesn’t mean you’re diversified if they all move together. True diversification requires low correlation between positions.

Understanding Correlation

Correlation coefficient ranges from -1 to +1:

- +1.0: Perfect positive correlation (always move together)

- +0.7 to +0.9: High correlation (usually move together)

- +0.3 to +0.7: Moderate correlation (sometimes move together)

- -0.3 to +0.3: Low correlation (independent movement)

- -0.7 to -0.3: Moderate negative correlation (often move opposite)

- -1.0: Perfect negative correlation (always move opposite)

Example of HIGH correlation (bad diversification):

| Token Pair | Correlation |

|---|---|

| JUP – RAY | 0.85 (both DeFi DEXs) |

| BONK – WIF | 0.92 (both meme tokens) |

| JTO – PYTH | 0.78 (both infrastructure) |

This portfolio appears diversified (6 different tokens) but isn’t. When DeFi or meme sentiment shifts, multiple positions move together.

Example of BETTER diversification (lower correlation):

| Token Pair | Correlation |

|---|---|

| SOL – BONK | 0.45 (moderate) |

| JUP – RENDER | 0.35 (low – different sectors) |

| PYTH – WIF | 0.20 (very low – oracle vs meme) |

Sector Diversification for Solana

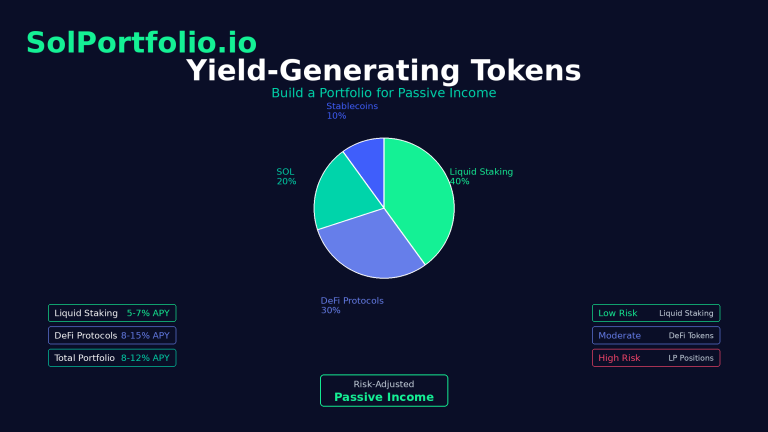

Major Solana sectors with different risk profiles:

- Base Layer (SOL): Lowest volatility, high liquidity

- DeFi (JUP, RAY, DRIFT, MNGO): Moderate-high volatility, protocol risk

- Infrastructure (PYTH, JTO, MOBILE): Moderate volatility, technical risk

- Meme (BONK, WIF, MYRO): Extreme volatility, narrative-driven

- NFT/Gaming (RENDER, TNSR): High volatility, market cycle dependent

- Liquid Staking (mSOL, jitoSOL): Low volatility, smart contract risk

Recommended allocation across sectors (moderate risk portfolio):

- Base Layer: 30-40%

- DeFi: 20-30%

- Infrastructure: 15-20%

- Liquid Staking: 10-15%

- Meme/Speculative: 5-10%

- NFT/Gaming: 5-10%

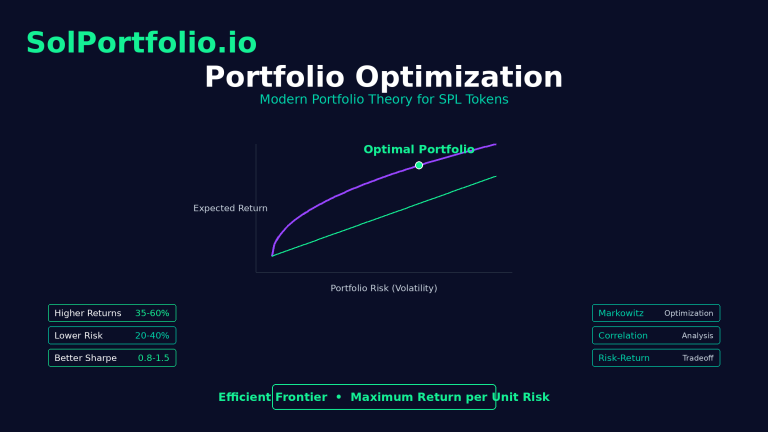

Markowitz Portfolio Optimization for Correlation

Manual correlation analysis is complex. Modern Portfolio Theory (MPT) uses mathematical optimization to find the allocation with the best risk-return tradeoff given historical correlations.

How it works:

- Calculate historical returns for each token

- Calculate correlation matrix between all token pairs

- Use quadratic optimization to find allocation minimizing volatility for target return

- Result: “Efficient frontier” showing optimal risk-return combinations

Why it matters: MPT automatically finds the portfolio with maximum diversification benefit. Instead of guessing which tokens are uncorrelated, the math tells you.

Automated approach: SolPortfolio.io implements Markowitz optimization and generates recommended allocations that maximize diversification benefit based on actual historical correlations.

🎯 Optimize Your Diversification

Stop guessing which tokens are uncorrelated. Markowitz optimization automatically finds the allocation with maximum diversification benefit.

SolPortfolio.io uses Modern Portfolio Theory to:

- ✓ Calculate correlation matrices across all your tokens

- ✓ Find optimal allocations on the efficient frontier

- ✓ Recommend truly diversified positions (not just many positions)

- ✓ Show expected risk reduction from better diversification

Free analysis • Based on historical correlations • Reduce risk 20-40%

Protocol Risk: Choosing Safe DeFi Platforms

If you’re using Solana DeFi protocols for staking, lending, or liquidity provision, protocol risk becomes your largest exposure.

Evaluating Protocol Security

Key questions to ask:

- Has the protocol been audited? By whom? (Top firms: Trail of Bits, OpenZeppelin, Kudelski)

- How long has it been live? Newer protocols = higher risk. Look for 6+ months live without incident.

- What’s the TVL (Total Value Locked)? Higher TVL = more battle-tested code, but also bigger target for hackers.

- Is there a bug bounty program? Active bug bounties mean security is prioritized.

- What’s the team’s track record? Anonymous teams = higher risk.

- Is the code open source? Allows community review.

Red flags (avoid these protocols):

- No audit from reputable firm

- Anonymous team with no track record

- Launched less than 30 days ago

- Unrealistic APYs (>100% on established tokens)

- No open source code

- History of exploits or bugs

Risk Mitigation Strategies

1. Diversify across protocols

Don’t put all DeFi exposure in one protocol. If you’re lending $50K, split it: $20K on Protocol A, $20K on Protocol B, $10K on Protocol C. If one gets hacked, you lose 40% not 100%.

2. Use only established protocols for large amounts

For positions >$10K, stick to protocols with:

- 12+ months live

- Multiple audits

- $100M+ TVL

- No historical exploits

3. Limit DeFi exposure to <50% of portfolio

Keep at least half your portfolio in simple wallet holdings (no protocol risk). This ensures one protocol failure can’t wipe you out.

4. Monitor protocol health

Watch for warning signs:

- Sudden TVL drops (capital fleeing)

- Governance disputes

- Team departures

- Security warnings from audit firms

Liquidity Risk: Ensuring Exit Capability

The best allocation is worthless if you can’t sell when needed.

Measuring Liquidity

Key metrics:

- Daily Trading Volume: Higher = more liquid

- Bid-Ask Spread: Difference between buy and sell prices. Lower = more liquid

- Market Depth: How much can trade before 1% price impact. Deeper = more liquid

Rule of thumb: Your position should not exceed 10% of average daily volume. If you hold $50,000 of a token, daily volume should be $500,000+.

Liquidity Tiers for Solana Tokens

Tier 1 (Highly Liquid – Safe for large positions):

- SOL: $2B+ daily volume

- JUP: $200M+ daily volume

- BONK: $100M+ daily volume

Tier 2 (Moderately Liquid – Safe for medium positions):

- RAY, PYTH, WIF: $20-50M daily volume

- Maximum position: 15% of portfolio

Tier 3 (Lower Liquid – Small positions only):

- Newer tokens: $5-20M daily volume

- Maximum position: 5-10% of portfolio

Tier 4 (Illiquid – Avoid or speculative only):

- <$5M daily volume

- Maximum position: 2% of portfolio if any

Managing Liquidity Risk

1. Front-load liquid tokens

Allocate largest positions to most liquid tokens. Your top 3 holdings should all be Tier 1 or Tier 2 liquidity.

2. Plan exits in advance

For illiquid positions, know your exit strategy:

- How many days to fully exit?

- What price impact to expect?

- Are there alternative exit routes (OTC, different DEXs)?

3. Monitor liquidity changes

Liquidity can dry up during crises. A token with $50M daily volume can drop to $5M in a crash. Reassess liquidity quarterly.

4. Use limit orders for illiquid tokens

Market orders on illiquid tokens suffer massive slippage. Limit orders let you set price, though they might not fill immediately.

Active Risk Monitoring and Alerts

Risk management is not “set and forget.” Continuous monitoring is essential.

What to Monitor Daily

- Portfolio value: Track daily changes

- Individual token performance: Identify outliers

- Market-wide movements: Is everything down or just your portfolio?

What to Monitor Weekly

- Current allocation vs targets: Check drift

- Volatility metrics: Is risk increasing?

- Liquidity levels: Have any tokens become illiquid?

- Protocol TVL: Are DeFi positions secure?

What to Monitor Monthly

- Correlation changes: Are tokens becoming more correlated?

- Maximum drawdown: Is MDD increasing?

- Sharpe/Sortino ratios: Are risk-adjusted returns acceptable?

- Position sizes vs Kelly criterion: Should allocations change?

Risk Monitoring Tools

Essential tools for Solana risk management:

- SolPortfolio.io: Portfolio risk analytics, volatility tracking, correlation matrices, Sharpe/Sortino ratios, drift alerts, Markowitz optimization

- DeFiLlama: Protocol TVL tracking, risk monitoring, audit status

- Birdeye: Token liquidity data, volume analysis, price alerts

- CoinGecko/CoinMarketCap: Market data, volume tracking, price monitoring

- Nansen: Smart money flows, whale tracking (premium)

Setting up automated alerts:

- Price alerts: Notify when any token moves >15% in 24 hours

- Drift alerts: Notify when allocation drifts >20% from target (SolPortfolio.io offers this)

- Liquidity alerts: Notify when daily volume drops >50%

- Protocol alerts: Notify when TVL drops >30% in 7 days

Stress Testing Your Portfolio

How will your portfolio perform in various crisis scenarios?

Common Stress Test Scenarios

Scenario 1: General Crypto Bear Market

- SOL: -50%

- Large-cap DeFi: -60%

- Mid-cap tokens: -70%

- Meme tokens: -85%

Example portfolio impact:

- 30% SOL → Down 15%

- 30% DeFi → Down 18%

- 20% mid-caps → Down 14%

- 20% memes → Down 17%

- Total portfolio: -64%

Scenario 2: Solana-Specific Crisis

- SOL: -70% (network issue, exploit, regulatory)

- Solana DeFi: -80% (contagion)

- Infrastructure: -60%

- Memes: -90%

Scenario 3: DeFi Protocol Hack

- Affected protocol: -100% (total loss)

- Other DeFi: -30% (contagion fears)

- Non-DeFi: -10% (general risk-off)

Scenario 4: Liquidity Crisis

- All tokens: -40% average

- Illiquid tokens: -70% (can’t sell at any reasonable price)

- Slippage costs: Additional 5-15% on exits

Interpreting Stress Test Results

Questions to ask:

- Can you psychologically handle the worst-case scenario?

- Would any scenario force you to sell at a loss?

- Do you have emergency liquidity (stablecoins, fiat) to avoid forced selling?

- Would any position become effectively illiquid?

If stress test reveals unacceptable risk:

- Reduce concentration in most vulnerable positions

- Increase allocation to lower-volatility tokens (SOL, liquid staking)

- Keep 10-20% in stablecoins as dry powder

- Reduce or eliminate DeFi protocol exposure

- Improve diversification across sectors

Black Swan Protection Strategies

Black swans are unpredictable, extreme events (FTX collapse, Terra Luna implosion). While you can’t predict them, you can limit damage.

Strategy 1: Position Limits

Hard caps on allocation:

- No single token >20% regardless of conviction

- No single DeFi protocol >15%

- No single sector >40%

- Speculative positions <10% combined

Position limits ensure no single failure destroys the portfolio.

Strategy 2: Keep Dry Powder

Always maintain 10-20% in stablecoins or SOL.

Benefits:

- Provides buying power during crashes (buy when others panic)

- Reduces forced selling (you have liquidity buffer)

- Lowers overall portfolio volatility

- Gives psychological comfort during crashes

Strategy 3: Tiered Risk Allocation

Divide portfolio into risk tiers:

Tier 1 (Core – 40-50%): Ultra-safe, highly liquid

- SOL

- Liquid staking derivatives (mSOL, jitoSOL)

- Stablecoins

Tier 2 (Growth – 30-40%): Moderate risk, proven protocols

- Established DeFi (JUP, RAY)

- Infrastructure tokens (PYTH, JTO)

Tier 3 (Speculative – 10-20%): High risk, high reward

- Newer DeFi protocols

- Meme tokens

- Emerging sectors

Risk management by tier:

- Tier 1: Never sells in crashes (buy more if anything)

- Tier 2: Rebalances systematically

- Tier 3: Sells quickly if broken (cut losses fast)

Strategy 4: Regular Risk Audits

Quarterly risk review:

- Recalculate all risk metrics

- Stress test against new scenarios

- Review correlation matrix (has it changed?)

- Assess liquidity of all positions

- Check protocol security status

- Adjust allocations if risk exceeds tolerance

Real-World Risk Management Example

Case Study: Portfolio During March 2025 Correction

Portfolio A (No Risk Management):

- 60% in one emerging DeFi protocol (concentrated)

- 30% in correlated meme tokens

- 10% SOL

- No monitoring, no alerts

What happened:

- DeFi protocol suffered exploit → -100% on 60% position

- Panic selling affected all risk assets → memes -70%

- SOL held relatively well → -30%

- Total portfolio: -82%

Portfolio B (Proper Risk Management):

- 30% SOL (liquid, base layer)

- 25% established DeFi (diversified across 3 protocols)

- 20% infrastructure tokens

- 15% stablecoins (dry powder)

- 10% speculative (memes, new projects)

- Active monitoring with alerts

What happened:

- No single protocol had >10% → exploit affected only 8% of portfolio

- Low correlation → infrastructure tokens down only 20%

- SOL position buffered losses → -30% on 30% = -9% total

- Stablecoins unchanged → 0% on 15%

- Used dry powder to buy SOL at lows

- Total portfolio: -28%

- Recovery: Within 2 months (bought dip with stablecoins)

Result: Portfolio B suffered 54 percentage points less loss (-28% vs -82%) due to proper risk management. Portfolio A would need 455% gain to recover. Portfolio B needed 39% gain, achieved in 8 weeks.

KEY INSIGHT: Risk management doesn’t prevent losses—it prevents catastrophic losses that destroy capital permanently. A 28% drawdown is recoverable. An 82% drawdown is devastating.

Common Risk Management Mistakes

Mistake #1: Confusing Diversification with Risk Reduction

The error: “I hold 10 different tokens, so I’m diversified and safe.”

Why it’s wrong: If all 10 tokens are highly correlated (all memes, all DeFi, etc.), you have no real diversification. During corrections, they all drop together.

Solution: Check correlations. Use Markowitz optimization to ensure true diversification benefit.

Mistake #2: Ignoring Position Size

The error: “This token will 10x, I’ll put 50% of my portfolio in it.”

Why it’s wrong: Even if you’re right 80% of the time, the 20% where you’re wrong with a 50% position will wipe out years of gains.

Solution: Follow Kelly criterion guidelines. Cap any position at 25% maximum, regardless of conviction.

Mistake #3: No Exit Plan for DeFi

The error: Putting tokens in DeFi protocols without monitoring or exit triggers.

Why it’s wrong: Protocol hacks happen fast. By the time you notice, funds are gone.

Solution: Set alerts for TVL drops, audit status changes, and unusual activity. Know your exit process in advance.

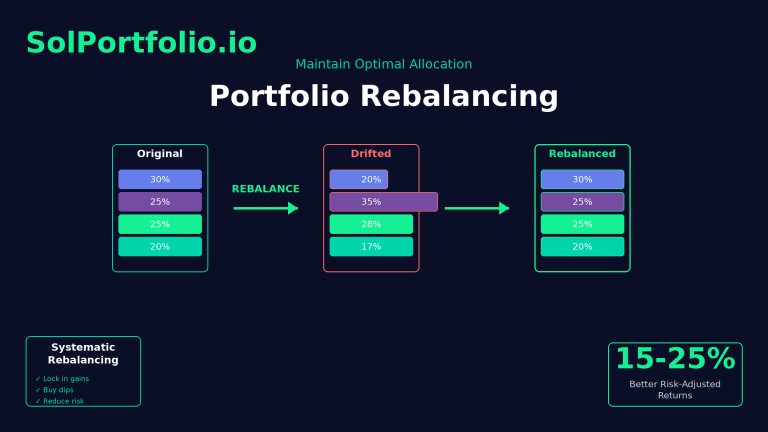

Mistake #4: Letting Winners Run Too Long

The error: Token goes from 10% to 45% of portfolio due to gains. You don’t rebalance because “it’s still going up.”

Why it’s wrong: You’ve turned a balanced portfolio into a concentrated bet. When (not if) it corrects, your portfolio crashes.

Solution: Rebalance systematically. Take profits on winners, redeploy to underweight positions.

Mistake #5: Anchoring to Entry Prices

The error: “I’ll sell when it gets back to my buy price” after a token drops 60%.

Why it’s wrong: Your entry price is irrelevant to future returns. You’re holding a losing position hoping for recovery that may never come.

Solution: Evaluate each position based on forward-looking prospects, not sunk costs. Cut losses when fundamentals deteriorate.

Frequently Asked Questions

Q: What’s an acceptable level of portfolio risk for Solana?

The Answer: It depends on your risk tolerance and time horizon. Conservative investors should target 30-50% annualized volatility with <30% maximum drawdown. Moderate investors can handle 50-100% volatility with 30-50% MDD. Aggressive investors accept >100% volatility and 50-70% MDD. Most importantly: your actual risk tolerance is revealed during crashes. If you panic sell, your risk was too high.

Q: How often should I check my portfolio’s risk metrics?

In Brief: Check daily portfolio value, but calculate detailed risk metrics (volatility, Sharpe, correlations) monthly. During high volatility periods or market crashes, increase monitoring to weekly. Set automated alerts for major drift (>20% from targets) or liquidity changes so you don’t need to check constantly.

Q: Should I sell everything during a market crash?

The Answer: No. Panic selling locks in losses at the worst prices. If you’ve done proper risk management (position sizing, diversification, dry powder), your portfolio is sized for your risk tolerance. The crash shouldn’t destroy you. Better strategy: hold or even buy with dry powder (stablecoins). Markets recover. Panic sellers don’t.

Q: How do I know if my portfolio correlation is too high?

In Brief: Calculate the average pairwise correlation across all holdings. If average correlation is >0.7, diversification benefit is minimal. Target average correlation of 0.3-0.5 for good diversification. Use SolPortfolio.io’s correlation matrix to identify highly correlated pairs and replace with lower-correlation alternatives.

Q: Is it safe to use leverage on Solana DeFi?

The Answer: Leverage amplifies both gains and losses. For experienced traders only. If you use leverage: (1) Never exceed 2x for Solana assets due to extreme volatility, (2) Set strict liquidation stop-losses, (3) Limit leveraged positions to <20% of portfolio, (4) Monitor daily, (5) Understand liquidation mechanics completely. For most investors, leverage adds unacceptable risk.

Q: What percentage should I keep in stablecoins?

In Brief: Minimum 10%, ideally 15-20% for active portfolios. Stablecoins provide: (1) Dry powder to buy crashes, (2) Liquidity buffer preventing forced sales, (3) Volatility reduction, (4) Psychological comfort. During bull markets, investors reduce stablecoins to chase gains. During crashes, they wish they had more.

Q: How do I calculate my portfolio’s correlation matrix?

The Answer: (1) Export 90 days of daily prices for all tokens, (2) Calculate daily returns for each token, (3) Use Excel’s CORREL function or Python’s pandas.corr() to compute correlations between all pairs. Or use SolPortfolio.io which calculates and visualizes correlation matrices automatically for your portfolio.

Q: Should I use the same position size for all tokens?

In Brief: No. Position size should reflect confidence level and risk. High-confidence, low-volatility tokens (SOL) can be 20-30%. Medium-confidence tokens should be 10-15%. Speculative positions should be 2-5%. Equal weighting ignores risk differences between tokens and results in excessive risk concentration in volatile positions.

🛡️ Start Professional Risk Management Today

Join thousands of Solana investors using institutional-grade risk analytics to protect their portfolios while maximizing returns.

✓ No credit card required • ✓ Connect wallet in 30 seconds • ✓ Free risk analysis

Conclusion: Risk Management as Competitive Advantage

In Solana’s extreme volatility environment, risk management isn’t about avoiding opportunity—it’s about surviving long enough to capture opportunity. The difference between professional and amateur investors isn’t stock picking ability. It’s risk management discipline.

The harsh reality: A portfolio that gains 200% but then loses 80% nets only 40% gain. A portfolio that gains 80% consistently without catastrophic drawdowns doubles every two years. Slow and steady wins.

Key principles:

- Position sizing > Token selection: Right size of wrong token beats wrong size of right token

- Correlation matters more than count: 5 uncorrelated tokens > 10 correlated tokens

- Liquidity is risk: Illiquid positions are forced holds regardless of fundamentals

- Monitor constantly: Risk metrics change; quarterly reassessment is minimum

- Prepare for black swans: Position limits and dry powder protect against unknown unknowns

The path forward:

- Calculate your current risk metrics (volatility, MDD, Sharpe, correlations)

- Assess if current risk matches your tolerance

- Implement position limits (no token >20%, speculative <10%)

- Diversify across sectors with low correlation

- Maintain 15-20% stablecoins for dry powder

- Set up automated monitoring and alerts

- Conduct quarterly risk audits

- Rebalance systematically when drift exceeds 20%

🚨 Never Miss Critical Risk Signals

Manual monitoring is prone to errors. Automated alerts catch problems before they become catastrophic.

Set up smart risk alerts:

- 📉 Portfolio volatility exceeds your threshold

- ⚠️ Allocation drifts >20% from targets

- 📊 Sharpe ratio degrades significantly

- 🔗 Correlation increases (losing diversification)

Join thousands of investors protecting their portfolios with automated monitoring

Risk management isn’t exciting. There are no 10x overnight stories. But there are investors who survive bear markets, capitalize on opportunities, and compound wealth over years. That’s the real alpha.

The Solana ecosystem offers unprecedented opportunity. With proper risk management, you capture that opportunity without the catastrophic losses that destroy most crypto portfolios. It’s not about eliminating risk—it’s about taking calculated risks with defined limits.

Start managing risk today. Your future self will thank you.

About SolPortfolio.io

SolPortfolio.io provides institutional-grade portfolio risk analytics for Solana investors. Connect your wallet to instantly calculate volatility metrics, Sharpe and Sortino ratios, correlation matrices, and maximum drawdown analysis. Get automated drift alerts, Markowitz-optimized allocation recommendations, and comprehensive risk reports. Built by quantitative finance professionals, SolPortfolio.io brings professional risk management tools to individual investors.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or risk management advice. Cryptocurrency investments carry substantial risk including potential loss of principal. Risk management strategies reduce but cannot eliminate risk or guarantee profits. Past performance and historical volatility do not guarantee future results. Always conduct your own research and consider consulting with licensed financial professionals before making investment decisions. Only invest capital you can afford to lose entirely.